Your

2026 benefits

Continuing care and

prescriptions

If you have upcoming or ongoing medical care or prescription needs, support is available to help you understand your options and navigate Transition of Care, Continuity of Care for serious or complex conditions, active prior prescription authorizations,

and any step therapy requirements. Use the links below to get started:

Plans at a glance.

Some plans cost more each month but cover more when you need care—others have lower monthly costs but you’ll pay more out of pocket when you use them. Have a look.

2026 Medical Plan Overview

Compare plans side by side—see what they cover, what they cost, and what sets them apart.

Flexible Spending Account (FSA) - for eligible healthcare or dependent care expenses. HSA (Health Savings Account) - for qualified medical expenses if enrolled in an HDHP.

HSA (Health Savings Account) - for qualified medical expenses if enrolled in an HDHP. HRA (Health Reimbursement Arrangement) - an employer-funded account that reimburses you for qualified medical expenses.

Limited Purpose FSA (LPFSA) - can be used alongside an HSA (limited to covering eligible dental and vision expenses.)

embedded

embedded

embedded

embedded

embedded

embedded

(no deductible)

(no deductible)

(no deductible)

**90-day mail order out-of-pocket amounts can be found through ExpressScripts by Evernorth (ESI). Specialty medications not covered by mail order.

*** Kaiser (CA only) plan designs have slight variations from the plans outlined above. Click here for more information.

2026 Dental Plan Overview

2026 Vision Plan Overview

2026 costs per paycheck

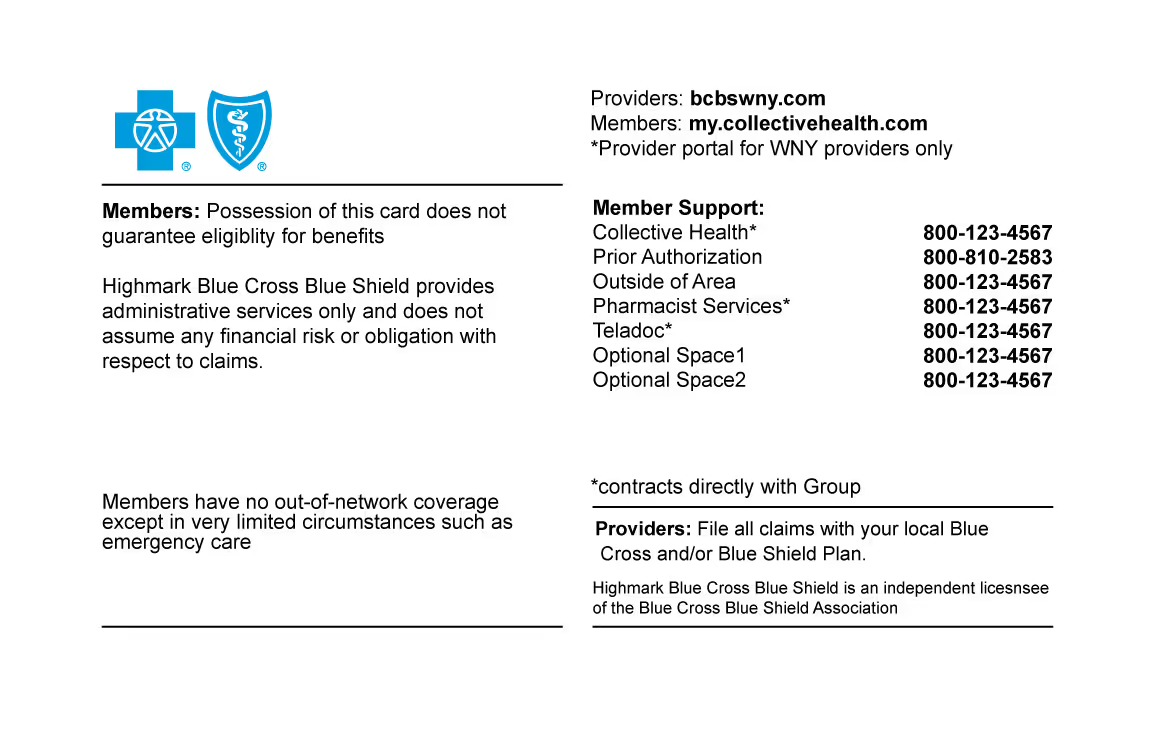

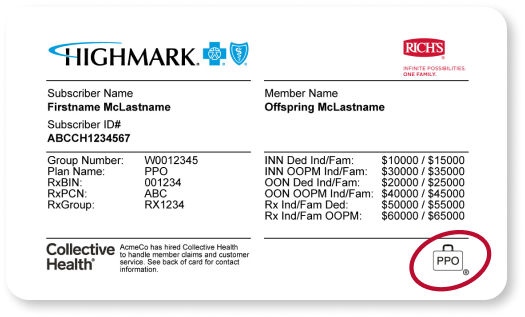

Benefits of the BlueCard® Suitcase

Collective Health has everything you need when it comes to understanding the benefits of your Highmark BCBS ID Card. The suitcase symbol means you have access to doctors and hospitals nationwide, all within the Blue Cross Blue Shield network.

To find in-network providers:

- Register or log in at my.collectivehealth.com

- Select the “Get Care” tab at the top of the page, where you can access the most up-to-date network and provider information for your plan.

Take care of your body, mind, and wallet

Wellbeing is about feeling your best today and preparing for the future. This year, Rich’s makes it easier than ever to focus on the areas that matter most, while earning rewards and support along the way.

We’re here to help.